Futures Market: Overnight, LME copper was closed. The SHFE copper 2507 contract opened at 77,740 yuan/mt overnight, reaching a high of 78,340 yuan/mt and a low of 77,710 yuan/mt during the session. The closing price was 78,150 yuan/mt. The overall trend fluctuated upward. The price increase was 0.31%, with a trading volume of 26,894 lots and an open interest of 157,842 lots.

[SMM Copper Morning Meeting Summary] News: (1) On May 23 (Friday), Polish Finance Minister Andrzej Domanski stated that under the new system, Poland's copper mining tax would be reduced starting next year. The mineral extraction tax, which includes copper, was introduced in 2012. According to the annual report of KGHM, Poland's largest copper miner, the company paid 3.87 billion zlotys in taxes in 2024. Domanski said that the tax cuts and the introduction of investment expenditure deductions would reduce tax revenue by approximately 10 billion zlotys ($2.66 billion) over ten years and lower costs for copper producers by the same amount.

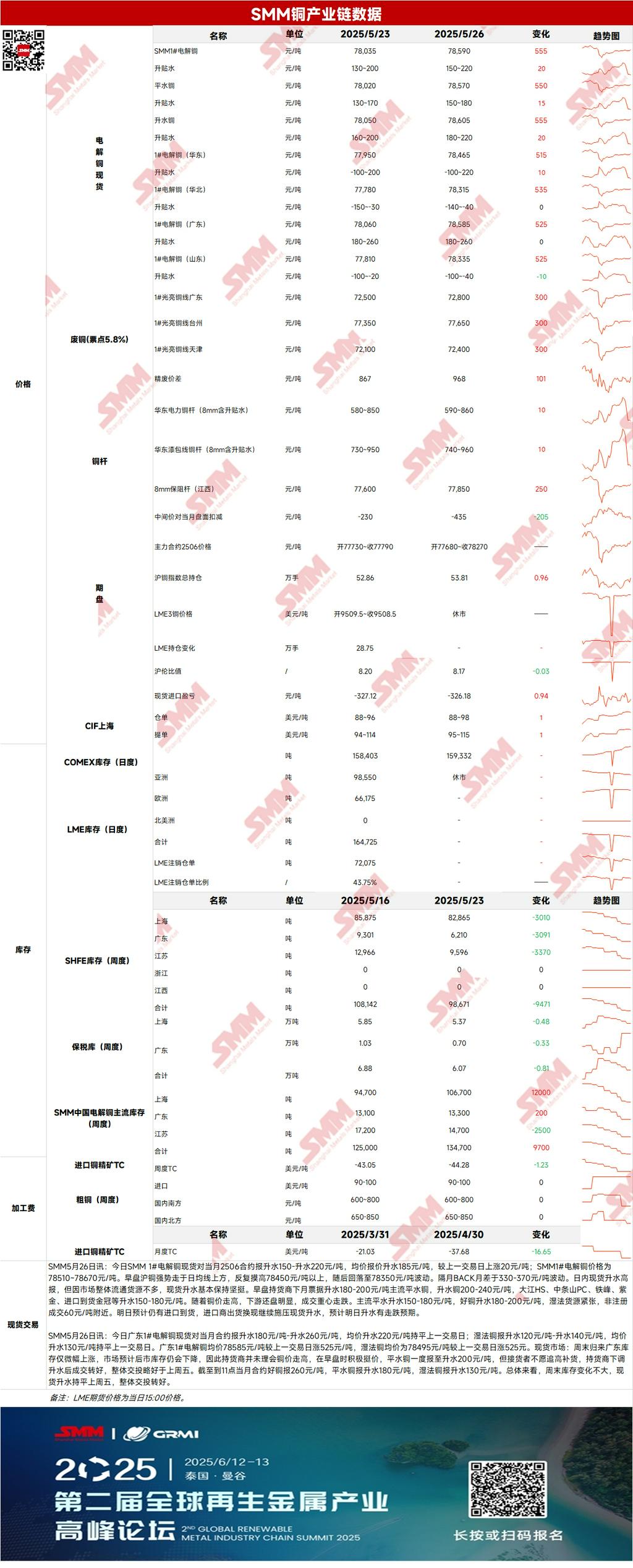

Spot: (1) Shanghai: On May 26, SMM #1 copper cathode spot premiums against the front-month 2506 contract were reported at 130-200 yuan/mt, with an average premium of 165 yuan/mt, up 30 yuan/mt from the previous trading day. The SMM #1 copper cathode price was 77,930-78,140 yuan/mt. In the morning session, the SHFE copper 2506 contract rose from around 77,800 yuan/mt to 78,000 yuan/mt, briefly touched 78,030 yuan/mt, and then pulled back, closing at 77,890 yuan/mt in the morning. The price spread between futures contracts (BACK) for the next month returned to the 300-330 yuan/mt range, with the center of spot premiums rising. Currently, there are signs of the price spread widening. Next week, as trading for cargoes with invoices dated next month begins, some traders may have cash flow needs. However, the price spread between front-month and next-month invoices is expected to be 30-40 yuan/mt. It is anticipated that next week's premiums and discounts will stabilize around this week's center. If they fall below 100 yuan/mt, the market may show purchase sentiment.

(2) Guangdong: On May 26, Guangdong #1 copper cathode spot premiums against the front-month contract were reported at 180-260 yuan/mt, with an average premium unchanged from the previous trading day at 220 yuan/mt. SX-EW copper premiums were reported at 120-140 yuan/mt, with an average premium unchanged from the previous trading day at 130 yuan/mt. The average price of Guangdong #1 copper cathode was 78,585 yuan/mt, up 525 yuan/mt from the previous trading day, while the average price of SX-EW copper was 78,495 yuan/mt, also up 525 yuan/mt from the previous trading day. Overall, inventory changes over the weekend were relatively small, and spot premiums remained unchanged from last Friday, with overall trading improving.

(3) Imported Copper: On May 26, warrant prices were at $90-98/mt, with a QP of June, and the average price was unchanged from the previous trading day. B/L prices were at $102-118/mt, with a QP of June, and the average price was unchanged from the previous trading day. EQ copper (CIF B/L) prices were at $73-83/mt, with a QP of June, and the average price fell by $1/mt from the previous trading day. Quotations referenced cargoes arriving in late May and early June. Overall, domestic copper is still expected to dominate arrivals in the latter half of the month, with relatively few non-registered spot orders. However, given the poor SHFE/LME price ratio, there is still expected to be downside room for subsequent premiums.

(4) Secondary copper: On May 26, the price of secondary copper raw materials remained unchanged MoM. The price of bare bright copper in Guangdong was 72,400-72,600 yuan/mt, unchanged from the previous trading day. The price difference between copper cathode and copper scrap was 867 yuan/mt, down 120 yuan/mt WoW. The price difference between copper cathode rod and secondary copper rod was 945 yuan/mt. According to an SMM survey, importers of secondary copper raw materials in Ningbo reported a slight increase in the supply of secondary raw materials this week. As LME copper prices pulled back below 9,600 yuan/mt during the week, many suppliers were concerned about widening losses from price declines, leading to a slight increase in shipments this week. Additionally, regarding the entry of US copper scrap into China through transshipment or exchange, traders stated that they had not heard any related news for the time being. It is expected that the import data for US secondary copper raw materials will show a significant pullback starting from May's data.

(5) Inventory: On May 26, the LME was closed, and copper cathode inventory decreased by 0 mt to 164,725 mt. On the same day, SHFE warrant inventory decreased by 573 mt to 32,833 mt.

Price: On the macro front, the fourth round of tariff negotiations between Japan and the US is scheduled for the 30th. The Japanese government plans to utilize 900 billion yen in national funds to mitigate the impact of US tariffs. An EU spokesperson stated that the EU's proposal of "zero tariffs for zero tariffs" remains on the negotiation table in talks with the US. It is reported that the EU has plans to accelerate negotiations with the US. Meanwhile, the partial suspension of copper mining operations in Africa has supported copper prices. On the fundamental front, there is limited overall market liquidity, and spot premiums remain firm. It is expected that there will be import arrivals today, and importers' efforts to liquidate their holdings will continue to put pressure on spot premiums, which are expected to face downward pressure. Overall, with the advancement of tariff negotiations between Japan, the US, and Europe, and the continued pressure on the US dollar index due to Trump's comprehensive spending and tax cut proposals, it is expected that copper prices will continue to find support at the bottom today.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and should not rely on this information to replace their own independent judgment. Any decisions made by clients are unrelated to SMM.]